From 7 months to 7 days: 7 Rural Banks Slash Loan Approval Periods

FIRST+II Program, Ghana

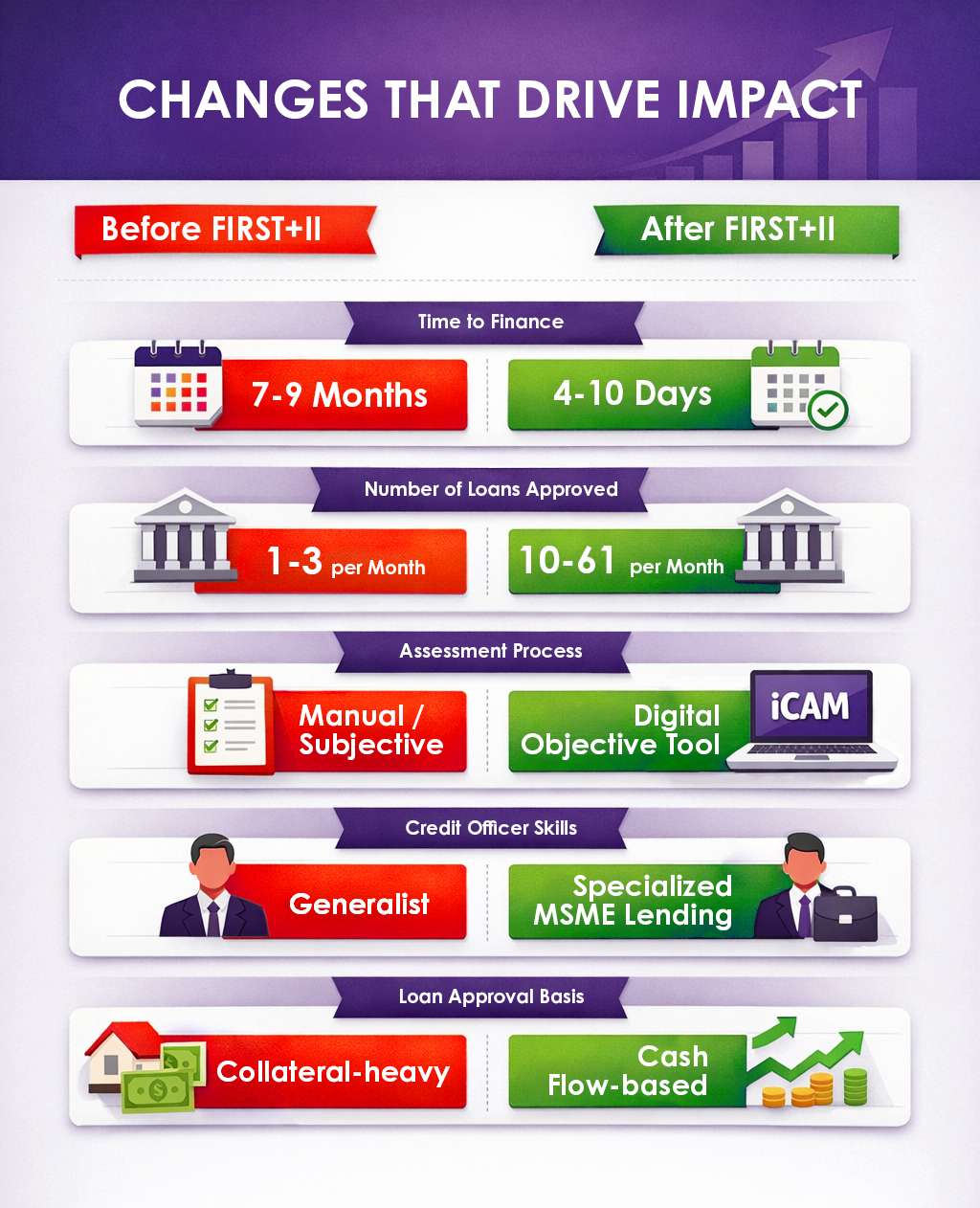

For decades, the journey for a Ghanaian smallholder farmer or a rural entrepreneur to obtain a bank loan was a marathon – the process could take more than 7 months from the first application to final disbursement. Ghanaian rural banks frequently require clients to build up savings deposits for 6 months, after which they may submit a loan application; banks then determine applicants’ repayment capacity based on their monthly savings. After applying for a loan, clients often wait another 3 to 8 weeks for their applications to be approved and disbursed, adding up to at least 7 months to access much-needed finance.

Because their money is tied up in the required savings account, prospective borrowers cannot use it for their businesses. For a farmer wanting to buy seeds before the rains or a trader needing inventory for a peak season, this delay can be a recipe for business failure.

Today, that narrative is changing. Under the FIRST+II program, a strategic partnership between CapPlus and the Mastercard Foundation, seven Ghanaian rural banks have successfully compressed that 7-month ordeal into a 7-day cruise to loan disbursements.

The FIRST+II Solution

The FIRST+II program was designed to solve systemic barriers such as these, and does so by delivering capacity building and technical innovation. The FIRST+II’s team designed and is now deploying an unsecured MSME loan product grounded in cash flow-based lending. While the model itself is not new, it is novel to most rural banks in Ghana.

CapPlus has also developed and installed the Integrated Creditworthiness Appraisal Module (iCAM) as the primary appraisal tool to assess borrowers’ ability and willingness to pay. iCAM is an automated system tailored for each bank that replaces the 6-month mandatory deposit with a thorough analysis of standard customer data that ensures quality appraisals, speed, equity and transparency. Credit officers are also well-trained in understanding iCAM’s assessments and borrowers’ financial situations.

Impact on Businesses, Women, and Youth

In the first four months of implementation, the seven banks achieved an average 6.8-day turnaround time from application to disbursement and loaned GHS 8.98 million to 438 farmers and businesses. Women and youth especially benefit since they tend to have less collateral and savings: women received 74% of the loans and 66% of the total loan value, and youth received 33% of the loans and 23% of the total loan value. By reducing the waiting period, banks have also seen a surge in first-time borrowers, especially people younger than 36 years.

Read Next Story Driving Systemic Change in MSME Finance

Atwima Kwanwoma Community Bank (AKCB), Ghana

For many Ghanaian rural and community banks, the challenge in delivering micro and small business (MSME) finance is building the systems, structures, and capabilities required to safely and sustainably lend to borrowers who may not have formal business records and practices.

Atwima Kwanwoma Community Bank took the opportunity to address its operational constraints by participating in the FIRST+II program implemented by CapPlus in partnership with the Mastercard Foundation.

In less than two years, AKCB has instituted significant systemic changes that increase its capacity to successfully lend to MSMEs, as it completed the following:

- Established a dedicated Business Development Unit to proactively identify and serve MSMEs

- Strengthened credit processes – including enhancing its loan appraisal practices – to responsibly lend to previously underserved customers

- Equipped bank staff with practical skills in credit management, marketing, and business development

- Refined and updated its reporting systems to improve how data is captured, analyzed, and applied, enabling it to more rapidly and effectively monitor performance, manage risk, and guide strategic decisions.

“Before this support, we did not have a business development department. Today, we have a fully functional unit driving our growth, and within just one year, we have increased our loan portfolio by over 80%. More importantly, we are now lending better, reaching MSME clients who previously would not have qualified and are doing so in a more structured and sustainable way,” Samuel Bonsu Sekyere, CEO, Atwima Kwanwoma Community Bank.

AKCB’s internal improvements are generating a positive impact far beyond its walls as it is now investing at least 80% more into local entrepreneurs who are growing their businesses, creating new jobs, and paying their workers more livable wages.

Read Next Story From Milestone to Momentum

Manya Krobo Community Bank, Ghana

Eight months into piloting an unsecured loan product that Manya Krobo Community Bank designed in partnership with CapPlus, under the FIRST+II program, the pilot has already exceeded expectations. What began as a bold step toward strengthening the bank’s MSME lending capacity is now delivering remarkable results – Manya Krobo has disbursed loans of over GHs3.82 million to 171 MSMEs across four pilot branches.

This remarkable performance reflects the product’s tailored design for rural MSMEs as well as the bank’s increasing confidence, agility, and efficiency. By streamlining the bank’s lending processes, introducing an automated loan appraisal system, and intensively training and mentoring bank staff on risk management, credit appraisals, and portfolio monitoring, CapPlus has empowered Manya Krobo to serve MSMEs – especially youth- and women-owned enterprises – more effectively than ever.

Branch managers are elated with the results, highlighting both the speed and quality of the new loan processes. The enthusiasm across the bank is palpable as teams apply the lessons, tools, and confidence gained so far from the pilot to scale inclusive MSME financing even further.

More importantly, each disbursement tells a story of an enterprise now able to grow, new opportunities created for workers, and a bank transformation made tangible. As the pilot continues, the bank is poised to prove that with the right systems, skills, and spirit, delivering credit to previously underserved MSMEs and smallholder farmers is a clear path for institutional growth, sustainability, and impact.

Read Next Story